A tow call rarely goes wrong at a convenient time. It's usually dark, traffic is still moving, the shoulder is too narrow, and the customer is already upset before the truck even arrives. The operator has to control the scene, load the vehicle cleanly, avoid damage, get back on the road, and sometimes store that vehicle until the owner, shop, or insurer figures out the next step.

That's why tow truck insurance can't be treated like a generic commercial auto purchase. A towing business doesn't just drive. It takes custody of other people's vehicles, moves them in high-risk conditions, and often stores them afterward. One bad handoff between coverages can leave the tow company paying for a claim it thought was insured.

The most common confusion isn't whether a business has insurance. It's whether the right policy responds at the right moment. The core question is simple: what covers the job at dispatch, on the road, during loading, while the vehicle is on the hook, and after it's dropped in the yard?

Table of Contents

- Why Tow Truck Insurance Is Your Most Important Tool

- The Core Four Coverages for Every Towing Operation

- Essential Add-Ons for Specialized Towing Risks

- Permits Filings and Staying Road-Legal

- What Drives Your Tow Truck Insurance Premiums

- How to Lower Your Premiums Through Smart Risk Management

- The Right Way to Get Quotes and Bind Your Policy

Why Tow Truck Insurance Is Your Most Important Tool

A rollback, a wheel-lift, chains, straps, dollies, and lights all matter. But none of them keeps the business alive after a serious claim. Insurance does.

A night recovery on a busy interstate is a good example. The truck is exposed to traffic. The driver is exposed outside the cab. The customer's vehicle may already be damaged, which means every scratch, broken trim piece, or bent suspension part becomes an argument later. If the vehicle ends up in the lot overnight, the risk doesn't stop when the driver clocks out.

That's why towing is insured as a specialized class, not as ordinary business driving. The U.S. automobile towing industry is projected at $11.8 billion in 2026 with 39,745 businesses, according to IBISWorld's U.S. automobile towing industry data. That scale matters because carriers don't look at a tow truck like a plumber's van or a delivery pickup. They underwrite the type of towing, the vehicles in the fleet, and how the business operates.

Insurance is operating equipment

A tow operator can have a truck ready, drivers ready, and calls coming in, but if the coverage is wrong, one claim can hit from three directions at once:

- Damage to someone else on the road

- Damage to the customer's vehicle while being towed

- Damage to a customer vehicle after it reaches the yard

Each one can fall under a different policy.

Practical rule: If a tow company can't explain which policy applies at each step of a job, it probably has a gap.

A common trade example is a contractor-owned service van that breaks down on the shoulder. The tow company hooks it, transports it, and drops it at the operator's fenced lot after the repair shop closes. If the tow truck rear-ends another vehicle on the way, that's one problem. If the contractor's van is damaged while attached, that's a different problem. If catalytic converters are stolen overnight from the van while it sits in the yard, that's another one.

A lot of owners buy tow truck insurance as if the goal is satisfying a contract or getting on a rotation list. However, the primary goal is to survive the routine claim that turns expensive fast. In towing, the equipment handles the car. Insurance handles the financial wreckage when something goes sideways.

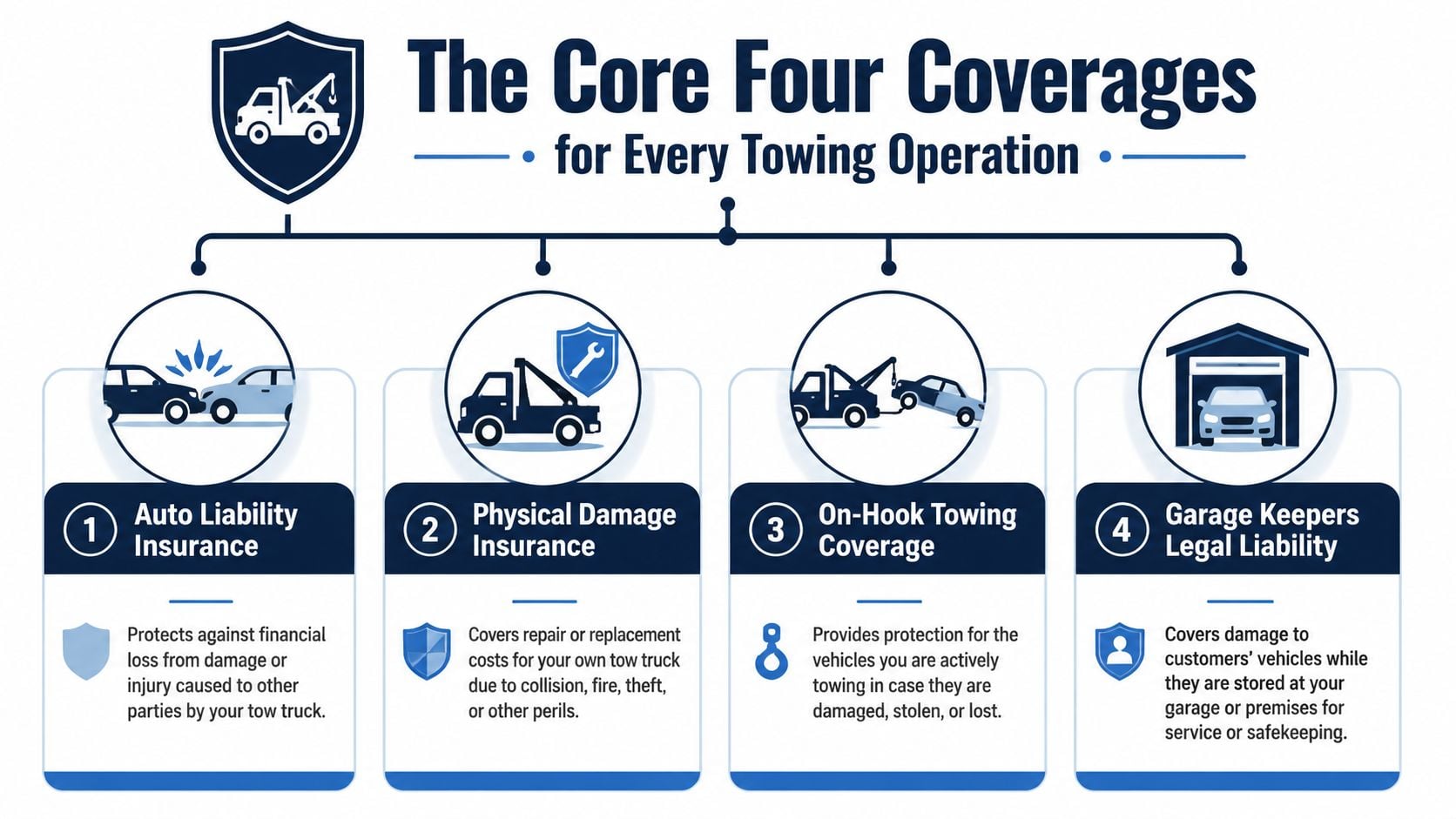

The Core Four Coverages for Every Towing Operation

Tow truck insurance works best when it's treated like a relay team. One policy doesn't run the whole race. Coverage hands off from one form to another as the job moves from roadway exposure to custody exposure to storage exposure.

Think in phases, not policy names

The biggest mistake is assuming commercial auto handles everything because the truck is involved. It usually doesn't.

According to Progressive Commercial's tow truck insurance overview, standard commercial auto often excludes the customer's vehicle, which is why towing operations typically need both on-hook towing and garagekeepers liability for non-owned vehicles in transit or in the operator's custody.

Here's the practical version.

Commercial Auto Liability handles damage or injury the tow truck causes to others. If the driver changes lanes and hits another car, this is the coverage that should respond. It protects against the truck's legal liability to third parties on the road.

Physical Damage covers the tow truck itself. If the rollback is damaged in a collision, stolen, or hit by a covered peril, this is the part that repairs or replaces the business's own vehicle, subject to the policy terms and deductible.

On-Hook Towing is built for the customer vehicle while it is actively being towed. If a strapped-down pickup shifts, a car door gets crushed during transport, or the towed vehicle is damaged while attached to the truck, this is the coverage owners need to look at first.

Garagekeepers Liability steps in when the customer vehicle is no longer being transported but is still in the tow operator's care, custody, or control at the business premises. Once the vehicle is in the yard, in a storage area, or parked at the shop awaiting pickup, that exposure usually belongs here, not under on-hook.

A tow job has phases. Road liability, active towing, and storage aren't the same risk, so they shouldn't be insured as if they are.

A useful way to think about it is this:

- The truck leaves the yard and drives to the call. That's road exposure.

- The operator loads and secures the customer vehicle. That begins active towing exposure.

- The vehicle reaches the destination or storage lot. That becomes custody and premises exposure.

Operators comparing limits should also understand how liability is expressed. A combined single limit policy explanation is worth reviewing because one number on a quote can look simple while hiding important differences in how losses are paid.

Core Towing Insurance Coverages Compared

| Coverage Type | What It Covers | When It Applies |

|---|---|---|

| Commercial Auto Liability | Injury or property damage caused by the tow truck to other people | During driving and roadway operations |

| Physical Damage | Repair or replacement of the tow truck itself after a covered loss | When the business's own truck is damaged |

| On-Hook Towing | Damage to a customer's vehicle while it is attached and being towed | From loading through active transport |

| Garagekeepers Liability | Damage to a customer's vehicle while stored or otherwise in the operator's custody on-site | After drop-off in the yard, lot, or garage |

A trade-specific example makes the handoff clear. A general contractor's box truck breaks down after hours. The tow company dispatches a heavy unit, loads the truck, and transports it back to the lot because the repair facility is closed. During transit, a strap issue damages the contractor's front axle. That points toward on-hook. Once the unit is parked overnight and a fire or theft loss hits while it sits in the fenced yard, that points toward garagekeepers.

General liability also matters, but in a different lane. It usually addresses premises and operations claims that don't fit the auto or custody forms. A visitor slipping in the office or yard waiting area is a different kind of claim than damage to a towed vehicle.

Owners who try to run a towing operation with only commercial auto are usually betting the whole shop on the wrong policy.

Essential Add-Ons for Specialized Towing Risks

The core four handle the backbone of the operation, but towing has edge cases that stop being “edge” cases once a claim hits. The side of the road is an unforgiving workplace, and many losses come from details outside the basic coverage stack.

Roadside work creates extra exposure

Uninsured and underinsured motorist coverage matters because tow operators work where traffic is close and mistakes happen fast. A driver can do everything right, set cones, wear high-visibility gear, and still get hit by someone who has no insurance or not enough of it. That problem isn't theoretical in roadside service. It's part of the job.

For owners, this is less about legal theory and more about business continuity. If a driver is injured by another motorist, weak recovery options can create pressure on the company from lost labor, scheduling disruption, and claim disputes.

Medical payments or similar injury-related options may also deserve a look depending on how the program is structured. The key is making sure roadside injury scenarios aren't treated as an afterthought just because the customer vehicle is the main focus.

Equipment, overflow, and higher-limit problems

On-hook covers the customer's vehicle while it's being towed. It does not automatically mean every piece of business property or every item related to the job is insured.

A heavy-duty operator may carry chains, dollies, specialty rigging, recovery tools, portable lighting, winching gear, and other mobile equipment that moves from truck to truck. If that gear is damaged, stolen, or disappears away from the main premises, owners often need to ask about inland marine or equipment coverage rather than assuming auto coverage will pick it up.

A practical trade example is a tow company hauling a commercial van for an HVAC contractor. The van itself may fall under the towing-related form during the transport phase, but the tools and mobile equipment inside can raise separate questions. That's the kind of claim where policy assumptions create fights.

If the business ever rents a truck during a breakdown, borrows equipment to cover overflow, or sends an employee on a company errand in a personal vehicle, hired and non-owned auto liability becomes important. Those vehicles can create liability for the business even when the company doesn't hold title to them.

For larger losses, some operators also need more ceiling above the primary policies. Reviewing how commercial umbrella insurance works helps when the operation handles heavier recoveries, municipal work, or jobs where one bad accident could cut through a primary limit faster than expected.

A smart coverage review for a tow company usually starts with one question: what gets used that isn't owned, what gets moved that isn't the truck, and what expensive problem could exceed the first layer of insurance?

Permits Filings and Staying Road-Legal

Insurance for a tow company isn't only about paying claims. It's also what keeps the business legally usable. If required filings aren't in place, the truck may be insured on paper but still useless for the work it needs to do.

What the filings actually do

State and federal filings connect the insurance policy to the government agency, permit authority, or contract requirement asking for proof. Depending on the operation, that may involve state-specific filings, municipal rotation requirements, or federal forms tied to interstate work.

For heavier for-hire towing, there's a federal floor that can't be ignored. Under FMCSA rules, for-hire tow trucks with a GVWR or GCWR of 10,000 pounds or more performing emergency moves in interstate or foreign commerce must maintain at least $750,000 in financial responsibility, as outlined by the FMCSA financial responsibility guidance for tow trucks.

That number matters because it isn't a pricing suggestion. It's a compliance threshold for qualifying operations.

Where operators get tripped up

Plenty of filing problems start with simple assumptions:

- The policy exists, so the filing must be done. Not always. A policy can be active while a required filing is still missing, delayed, or incorrect.

- A certificate solves everything. It doesn't. A certificate proves insurance exists, but it isn't the same as a statutory filing.

- One filing covers all work. It may not. Police rotation, municipal contracts, storage lots, and interstate moves can each bring their own paperwork requirements.

The policy is the engine. The filing is the license plate. One doesn't replace the other.

A contractor-focused tow example is a company that handles roadside breakdowns for fleet vans crossing state lines. The trucks are insured, but a filing issue holds up approval for contracted work. The result isn't just paperwork frustration. It can mean lost assignments, delayed starts, and awkward conversations with agencies or motor clubs.

Operators should also keep current certificates organized for customers, cities, lenders, and contract partners. A plain-English guide to a certificate of insurance template helps owners know what they're looking at when they review proof of coverage before sending it out.

What Drives Your Tow Truck Insurance Premiums

Tow truck insurance costs what it costs for a reason. This isn't a standard delivery fleet exposure. The business combines road risk, customer-vehicle damage risk, and often storage-lot risk in one operation.

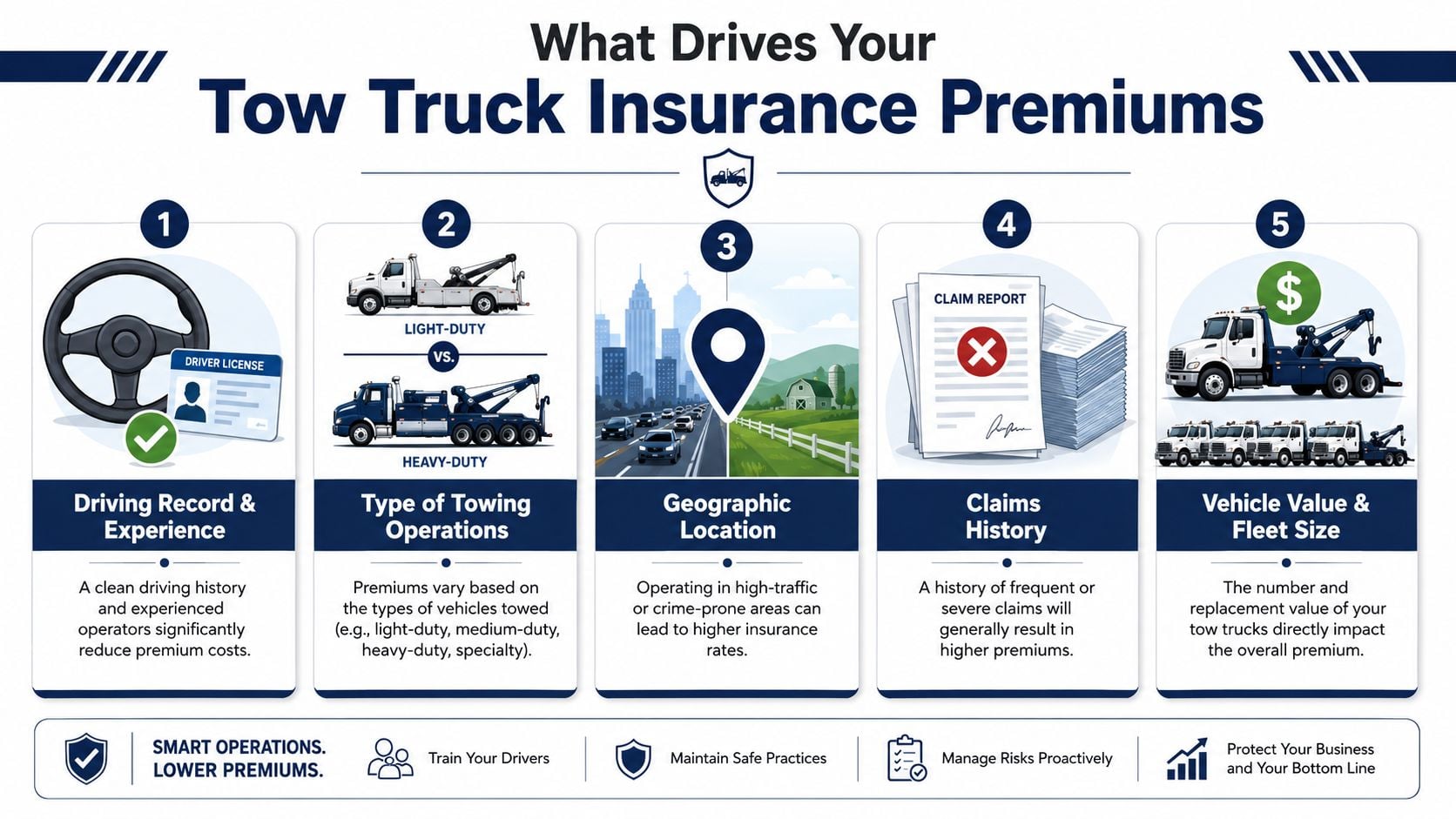

Your operation tells the underwriter the story

Underwriters usually start with what kind of towing the business does. Light-duty breakdown work isn't the same as heavy recovery. Police impound, repossession-related work, long-distance hauling, roadside assistance, private property towing, and municipal rotation all create different loss patterns.

Then they look at who is driving and what they're driving. Driver records matter. So does experience with towing-specific equipment. A large rollback operated by a seasoned driver and a wheel-lift handed to a new hire with a rough motor vehicle record are not the same account, even if both businesses have the same truck count.

The service area also matters. A wider operating radius means more miles, more time in traffic, more road conditions, and more chances for something to go wrong before the vehicle is dropped.

A practical example is a towing company that mainly serves local contractors, shops, and property managers inside one metro area versus an operator that handles emergency interstate recoveries and longer secondary moves. Even without quoting a rate, it's easy to see why the second profile draws tougher underwriting.

The market itself affects pricing

Pricing also reflects how many insurers want the business in the first place. The towing sector is viewed as high-risk by many insurers, and one broker noted that only “around 10 or so” carriers actively participate in the space, according to FreightWaves reporting cited by Reliance Partners on towing-sector insurance capacity. When fewer carriers compete, operators with blemishes on their record usually feel it first.

That market pressure shows up in published pricing snapshots too, but the more useful takeaway for an owner is this: availability and fit matter almost as much as price. A cheap quote with the wrong exclusions can become the most expensive option in the stack.

When reviewing options, a commercial auto policy quote guide can help owners organize the right underwriting details before they go to market. The cleaner and more complete the submission, the better the chance of getting a serious offer instead of a fast decline.

Underwriters price towing based on the jobs taken, the drivers hired, the vehicles used, and the way the company controls the scene after pickup.

Claims history stays in the middle of all of this. Frequent backing losses, customer-vehicle damage disputes, unsecured lots, or driver turnover can make an account harder to place. On the other hand, a disciplined operation with clean documentation gives the underwriter a reason to believe tomorrow won't look like the worst part of last year.

How to Lower Your Premiums Through Smart Risk Management

Most towing operators can't control the insurance market. They can control whether the account looks sloppy or disciplined. Over time, that distinction matters.

One market data point puts average commercial auto for towing businesses at about $737 per month, according to LogRock's tow truck insurance overview. That's enough to remind any owner that preventable claims cost money twice. First in the loss itself, then in the renewal that follows.

The habits that actually help

The strongest accounts usually do a few things well, consistently.

- Hire like every driver affects the whole fleet. One weak motor vehicle record can change how an underwriter sees the account. Screening should happen before keys are handed over, not after the first close call.

- Train for loading, not just driving. Many painful towing claims aren't highway pileups. They're bent suspensions, damaged fascias, scraped wheels, and bad securement decisions.

- Keep the lot controlled. Gates, lighting, camera coverage, key control, and limited after-hours access help reduce the kinds of storage-related claims that create expensive disputes.

- Maintain trucks on schedule. A blown tire, failed winch component, or lighting problem can turn a normal call into a liability mess fast.

A tow company that handles contractor vehicles is a good example. If operators routinely move service vans full of tools, equipment racks, and ladder setups, securement and intake discipline need to be tighter than average because the argument after a loss is rarely limited to the body panels.

Documentation saves arguments later

The best risk control in towing is often paperwork plus photos.

Before transport, many operators benefit from documenting the vehicle's condition at pickup, noting pre-existing damage, wheel condition, glass condition, and any obvious mechanical issue. After drop-off, a second round of photos can close the loop. That process won't prevent every claim, but it can stop a weak claim from becoming an expensive settlement.

A blurry memory loses to a clear intake form every time.

The same goes for theft prevention in stored vehicles. Operators managing impounds, contractor vans, or customer cars in a yard can pick up practical ideas from Quick Keys' car security guide, especially around layered vehicle-security habits that support what a fenced lot and key-control process are already trying to do.

Annual policy review matters too. If the business added heavier trucks, expanded into recovery work, changed storage practices, or hired younger drivers, the insurance program needs to match reality. Good risk management isn't glamorous. It's just what keeps a bad month from turning into a bad year.

The Right Way to Get Quotes and Bind Your Policy

Good tow truck insurance placement starts before the first quote request goes out. If the submission is incomplete, the answers are rushed, or the operation is described too loosely, the business usually gets weaker options.

Bring the right information up front

A serious quote process should include a clean vehicle schedule, driver list, description of operations, garaging address, operating radius, and details about whether the business handles storage, recovery, police rotation, private property towing, or contractor and fleet work. If the company stores vehicles, that needs to be stated clearly. If it performs interstate emergency moves, that matters too.

Owners should also be ready to explain prior losses in plain language. A claim history with context is easier to underwrite than a loss run dropped on the desk with no explanation.

A contractor-focused example would be a tow company that serves local electricians, plumbers, and HVAC fleets during breakdowns and after-hours moves. That account should say so directly. It helps the underwriter understand the pattern of work instead of guessing from broad labels.

Compare policy language, not just price

The cheapest quote can still be the wrong one. Owners should ask:

- What does the policy say about on-hook losses

- How does garagekeepers apply in the yard

- What deductibles apply to different claim types

- Are there sub-limits or exclusions that affect the work performed

- Are all required filings and certificates included or available

For business owners trying to understand the broader insurance buying process, this guide on how to get bonded and insured is a helpful plain-English reference.

There's also value in understanding the driver side of premium control. Some of the same behavioral factors that affect personal auto costs show up in commercial underwriting too, and this article on how to reduce your car insurance costs offers practical habits that translate well into fleet culture, especially around safer driving and long-term loss control.

Binding the policy is the last step, not the easy step. Before coverage is bound, the business should confirm effective dates, vehicle lists, driver lists, deductibles, payment terms, filing requirements, and who will issue certificates for contracts or rotation lists. Once the policy is active, all certificates and proof of insurance should be stored where office staff can send them quickly when a city, shop, lender, or contractor asks.

Tow truck operations don't have room for vague coverage. If the policy doesn't match the way the trucks are dispatched, loaded, towed, and stored, the gap usually shows up during a claim. Coverage Axis offers free quotes and coverage reviews for commercial operators who need a tow truck insurance program built around the actual sequence of risk, not a generic auto policy with the wrong labels.