A lot of small contractors hit the same wall at the same time. The business is finally moving, a helper is on the truck, a general contractor asks for a certificate, and suddenly workers comp stops feeling like paperwork and starts feeling like a test no one explained.

That confusion gets expensive fast. For contractors, workers comp for small business isn't just about meeting a legal requirement. It affects bids, hiring, subcontractor relationships, year-end audits, and whether one bad injury turns into a cash flow crisis. The contractors who manage it well usually aren't buying more insurance than everyone else. They're classifying labor correctly, controlling subcontractor paperwork, and keeping records clean enough that the audit doesn't become a fight.

Table of Contents

- Who Legally Needs a Workers Comp Policy in 2026

- Decoding Your Premium How Rates Are Set for Trades

- The Subcontractor Trap That Inflates Your Premium

- The Buying and Audit Process From Quote to True-Up

- What to Do When a Worker Gets Hurt on the Job

- Smart Loss Control Tactics to Lower Your Future Premiums

- Becoming a Lower-Risk Contractor Starts Now

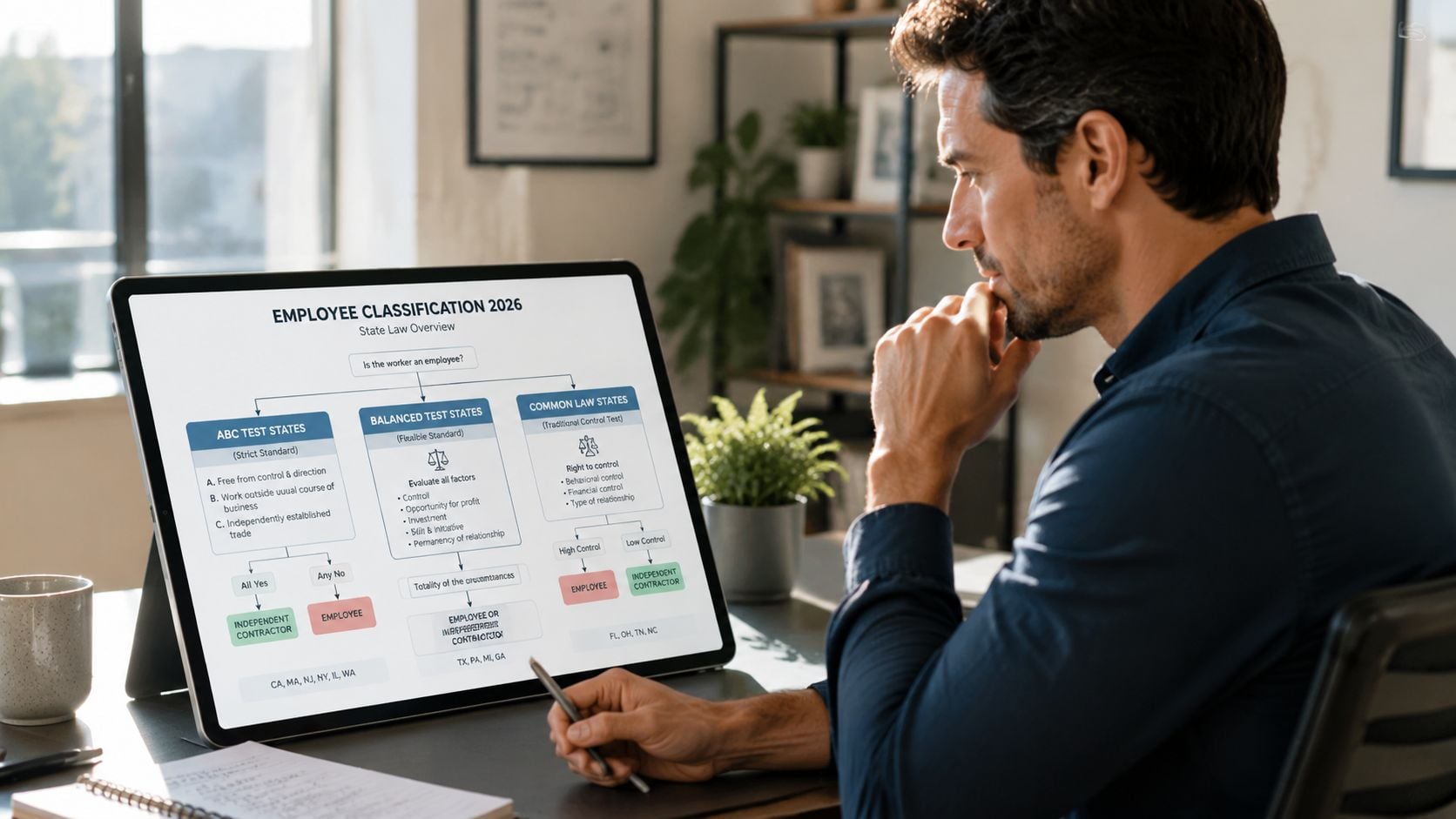

Who Legally Needs a Workers Comp Policy in 2026

A roofer adds one part-time helper for tear-offs on weekends. Then a GC asks for proof of workers comp before the next job starts. The roofer says the helper is "just part-time" and a cousin who gets paid when work is busy. The GC doesn't care. The state probably won't care either if that person is functioning like an employee.

Most states require workers' compensation when a business has one or more employees, and the financial stakes are serious because The Hartford notes that the average cost of a workers' compensation claim for accidents in 2022–2023 was $47,316. For a small trade shop, that kind of claim can do more damage than the annual premium ever would.

Employee status is broader than most contractors think

On paper, small operators often sort workers into easy labels. Employee. 1099. family help. day labor. sub. On a roof, in a trench, or on a framing site, those labels don't always hold up when a claim happens.

A worker who shows up on the contractor's schedule, uses the contractor's tools, performs the contractor's core trade work, and answers to the contractor's foreman can create employee exposure even if the check stub says something else. That catches a lot of contractors by surprise, especially when the worker is a family member or someone paid casually.

Practical rule: If a person is doing the contractor's regular field work under the contractor's direction, treating that person as outside the workers comp system is risky.

LLC status also doesn't solve this by itself. Being organized as an LLC or S-corp may matter for taxes and liability planning, but it doesn't automatically remove workers comp obligations for actual workers on site.

The common gray areas that trigger trouble

A small trade business usually needs a hard answer on these situations before hiring:

- Part-time labor: If the person is still an employee under state rules, part-time status won't make the exposure disappear.

- Family members: A son helping with gutter work or a spouse doing payroll are not automatically handled the same way. Field work and office work create different issues.

- Exclusive 1099 helpers: If one "independent contractor" only works for one contractor and performs the same trade labor as employees, that setup often gets challenged.

- Day laborers: These workers create some of the worst claim disputes because the documentation is usually weak right when the injury happens.

For contractors trying to understand where workers comp ends and employer injury liability begins, this is also where employers liability insurance becomes part of the conversation.

A roofer's real exposure

Take a two-crew roofing company. One owner, one payroll office employee, two regular installers, and one extra hand brought in during storm season. That extra hand may only work certain weeks, but the work itself is high hazard and directly tied to the contractor's operations. If he slips from a ladder, the argument that he was "just temporary" won't help much.

Contractors usually get into trouble here because they ask the wrong question. They ask, "Can this person be paid another way?" The better question is, "How would the state, carrier, or auditor classify this person after an injury?"

Decoding Your Premium How Rates Are Set for Trades

A lot of contractors look at a workers comp quote and assume the carrier pulled a number out of thin air. That isn't how it works. The price usually comes from a formula, and once a contractor understands the moving parts, bad classifications and bad estimates get easier to spot.

The basic structure is simple. Payroll multiplied by a classification rate, adjusted by an experience modification factor. Carrier minimums often start around $250 to $1,000 per year, and trade rates can run from under $1.00 to more than $10.00 per $100 of payroll depending on job risk, according to Canal HR's summary of workers comp pricing factors.

Why the same payroll can produce very different premiums

Take a plumbing contractor with two field techs and one office admin. The office employee sits at a desk, answers calls, and schedules jobs. The field techs cut pipe, crawl under structures, drive to sites, and work around tools and active construction zones.

Those wages should not live in the same bucket. Workers comp rates are built around the actual job duties tied to each class code. The contractor who throws everyone into one field class may overpay. The contractor who dumps field labor into clerical to make the quote cheaper is creating audit trouble.

A clean quote usually depends on separating labor by what people really do, not by what sounds convenient.

What each pricing piece means on a real job

Here's the practical version of the formula:

| Factor | What it means in the field |

|---|---|

| Payroll | Estimated wages for each type of worker |

| Class code | The trade risk assigned to that work |

| Experience mod | A claims-based adjustment that can move premium up or down |

| State factors | Local rating rules and policy requirements |

A contractor doesn't need to memorize rating manuals. The contractor does need to know whether the shop fabricator, field installer, project manager, and office admin have been grouped correctly.

A workers comp policy is part insurance policy, part payroll report. If the payroll side is sloppy, the premium side won't stay stable.

Where small contractors usually make mistakes

The biggest errors usually come from operations that have changed faster than the policy has. An HVAC company starts with service work, then adds new construction. A landscaping company starts doing tree work. A concrete contractor takes on demolition cleanup. The payroll may rise, but the bigger issue is that the risk profile changes.

The other common mistake is poor payroll allocation. If a worker splits time between shop, office, and field, the contractor needs defensible records. Without them, the auditor usually uses the more expensive class that matches the riskier work.

Contractors who want a better handle on how claims history affects price should understand the basics of the workers comp experience modification factor. That number isn't abstract. It becomes part of the bill.

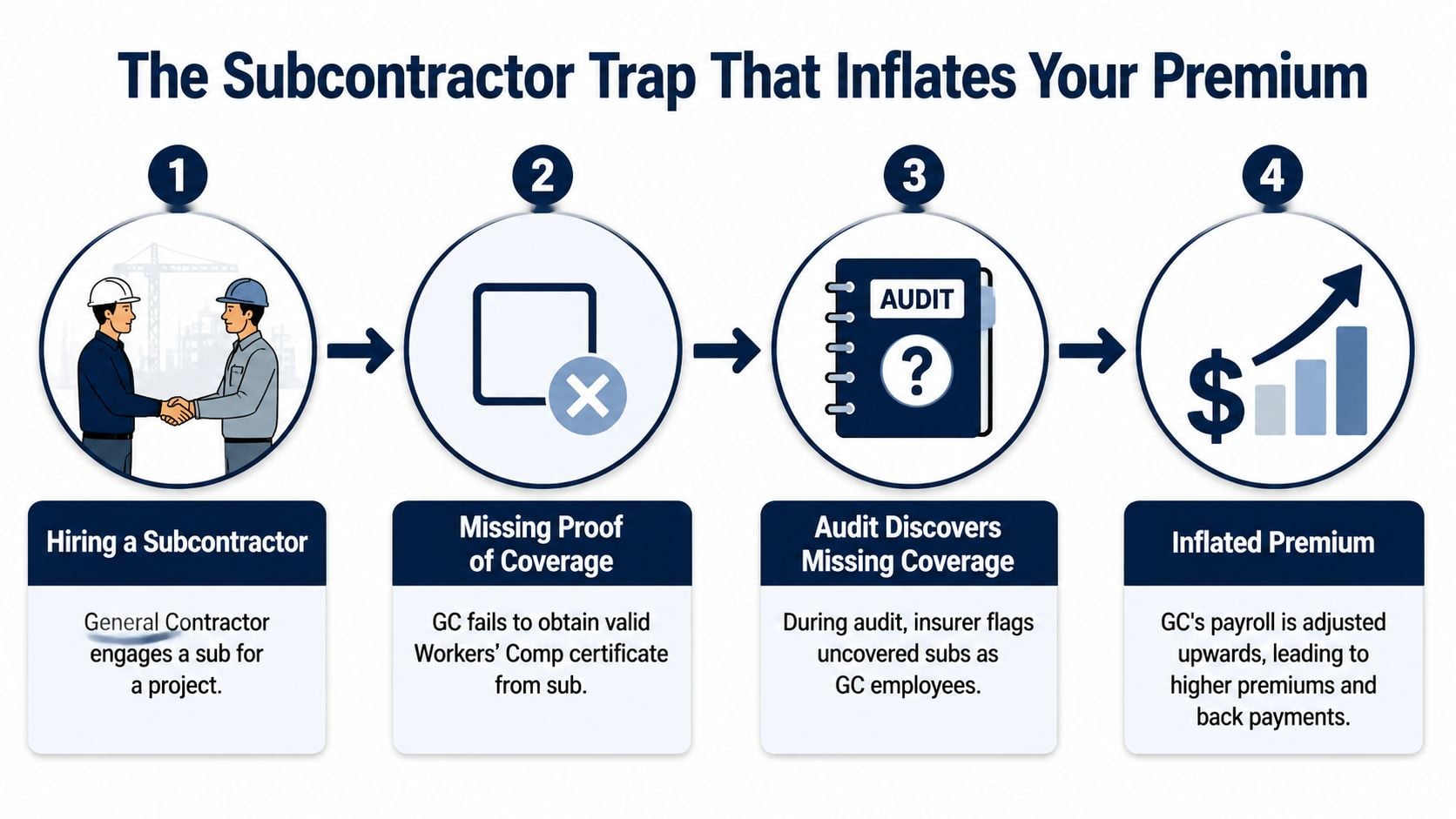

The Subcontractor Trap That Inflates Your Premium

A GC hires a framing crew for a fast commercial buildout. The sub says coverage is in place. The certificate never gets collected, or it gets collected once and never checked again. Months later, a worker gets hurt, the policy audit starts, and the GC finds out that "the sub had insurance" is not the same thing as having usable proof that the carrier will accept.

This is one of the most expensive blind spots in workers comp for small business. Contractors often separate subcontractor management from workers comp management. The carrier usually doesn't.

Why a subcontractor can still affect the contractor's policy

According to 2024 to 2025 industry data, 27% of contractor losses included subcontractor injury costs passed through to the primary carrier, and these payroll inclusion issues can inflate a GC's workers comp rates by 15% to 30% when a subcontractor's insurance is inadequate or unverified, based on the referenced 2024 National Association of Construction Insurers data in the verified brief.

That matters because the carrier may treat uninsured or unsupported subcontractor payroll as exposure belonging to the hiring contractor. Then the problem shows up in two places. First, the claim side. Second, the audit bill.

The certificate isn't the finish line. It's the starting document.

What a GC should actually verify

A lot of contractors collect COIs the same way they collect lien waivers. They just want the file to look complete. That approach fails when the certificate is expired, the named insured doesn't match the subcontract, or workers comp wasn't carried at all.

A better process looks like this:

- Match the legal name: The name on the certificate should line up with the subcontract agreement and the entity being paid.

- Check effective dates: A valid certificate at bid time doesn't help much if the work continues after expiration.

- Verify workers comp is shown: Some contractors glance at the page and assume all lines are present.

- Keep updated copies: Annual audits happen long after the project wraps. The contractor needs the paper trail then, not just during mobilization.

For firms that routinely hire specialty crews, a focused review of workers comp for subcontractors can help clarify what should be collected before labor ever hits the job.

A framing crew example

Say a GC hires an uninsured framing crew for a retail tenant improvement. The sub is cheap, available, and says he always works this way. During the audit, the carrier asks for workers comp certificates. There aren't any. The carrier may include that labor cost in the GC's premium basis because the exposure wasn't properly transferred or documented.

Contractors often get frustrated, but the carrier's logic is straightforward. If the sub's workers are doing trade work on the project and no valid workers comp trail exists, the carrier assumes the exposure may fall back on the hiring contractor.

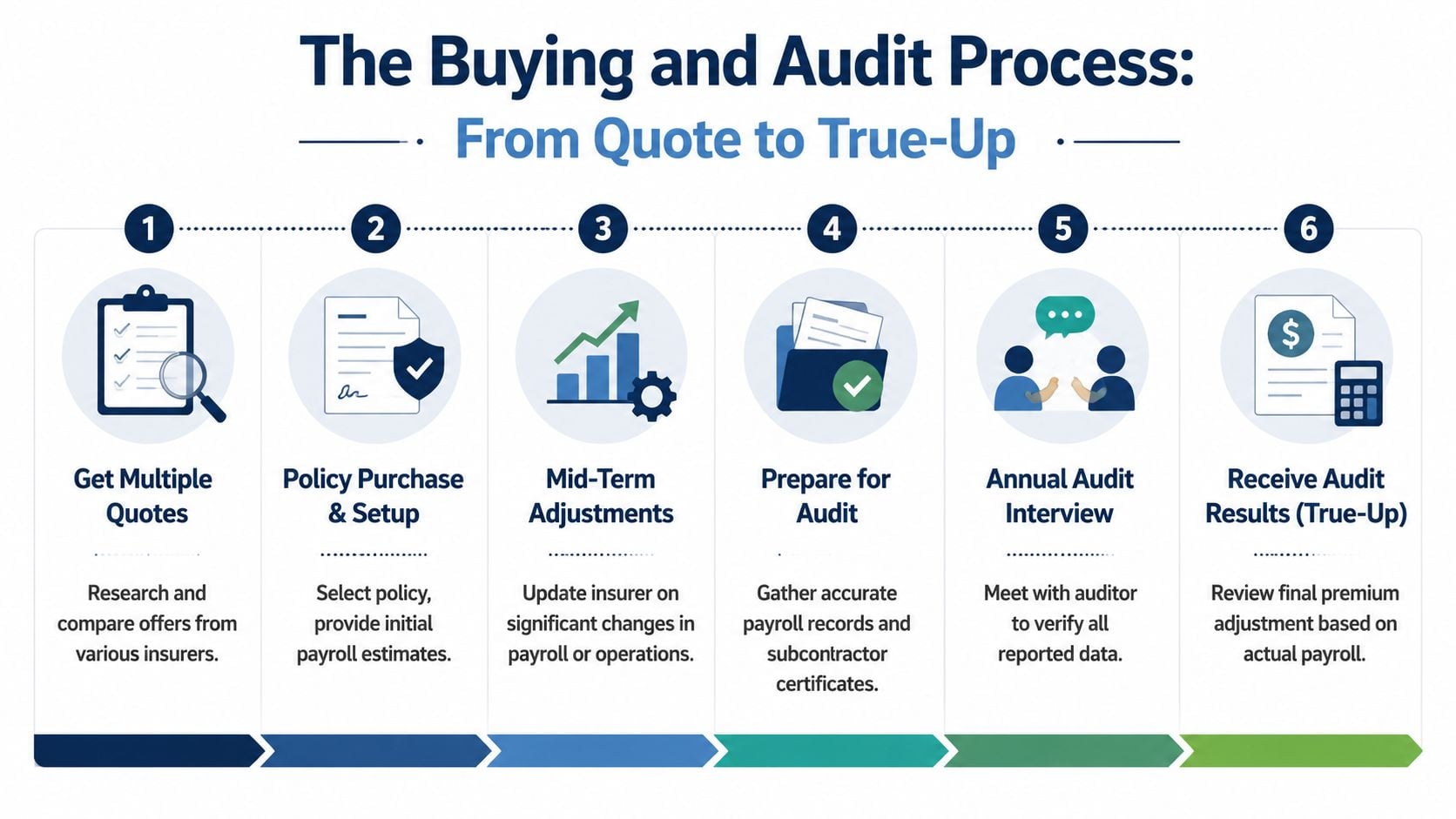

The Buying and Audit Process From Quote to True-Up

The easiest workers comp audit is built months before the auditor calls. Contractors who treat the quote as a rough guess usually end up treating the audit as damage control. Contractors who build the policy on clean data usually get a much smoother true-up.

An electrician is a good example. One crew handles service calls, one helper works part-time, and occasional labor is subcontracted during busy periods. If that contractor can show estimated payroll by job type, current certificates for subs, and clean books, the policy starts right and the audit usually stays manageable.

What to gather before asking for a quote

A useful quote usually requires more than a total annual payroll number. The advisor or underwriter will want a real picture of operations.

That normally includes:

- Payroll broken out by job type. Office staff, field labor, shop work, and owners shouldn't be blended if their duties differ.

- A description of the work performed. "Electrical contractor" is too broad if the company does service, new construction, and low-voltage work.

- Subcontractor cost details. Not every dollar paid to subs is treated the same way.

- Prior loss history if available. Clean reporting matters more than polished storytelling.

For contractors that need a better process for collecting and storing proof from subs, a plain certificate of insurance template can help standardize the file before the audit starts.

Why the audit surprises so many owners

At the start of the policy, payroll is estimated. At the end, the carrier compares the estimate to what happened. That's the true-up. If payroll rose, class codes changed, or uninsured subcontractor costs were left unsupported, the final premium can move.

A lot of small contractors create the problem themselves by mixing labor costs in one ledger line or failing to maintain separate records for office and field staff. When the auditor can't verify the lower-rated category, the contractor loses that benefit.

Keep records like someone will review them after a claim, after a busy season, and after a bookkeeper change. Because someone will.

The file that makes audits easier

A contractor doesn't need a perfect back office. The contractor needs a consistent one.

The year-round audit folder should usually include:

- Payroll journals

- Quarterly tax reports

- Detailed job descriptions

- Subcontractor invoices

- Current and historical COIs

- Owner and officer payroll records where applicable

For a well-run electrical contractor, the audit often becomes a short reconciliation instead of a drawn-out dispute. The same policy, with the same carrier, can feel either routine or painful depending on whether the records tell a clear story.

What to Do When a Worker Gets Hurt on the Job

An outdoor contractor's employee lifts a wet paver, twists hard, and goes down with a back injury. The crew freezes for a second because everyone is thinking about production, schedule, and whether the employee can stand up. That pause is where small mistakes start.

The first job is medical care. If emergency treatment is needed, get it moving immediately. Then secure the area, stop similar work if the hazard is still active, and document what happened while details are still fresh.

The first day matters most

The employer should gather the basic facts early. Who was involved, what task was being performed, what equipment was being used, who saw it happen, and whether there were photos of the scene. Waiting until the next morning usually means details get blurred.

The carrier will also need prompt notice. Contractors create extra friction when they delay reporting because they hope the worker will "shake it off." If the injury turns into lost time or medical treatment, late reporting tends to make the claim harder for everyone.

A simple response sequence helps:

- Get treatment started: The worker's health comes first.

- Preserve the scene if needed: Especially if equipment, footing, or material handling may have contributed.

- Report the injury internally: Supervisor notes should be factual, not argumentative.

- Notify the carrier quickly: Delay rarely helps.

- Stay in contact with the worker: Silence is where distrust grows.

The hidden danger with 1099 labor

The most painful claims often involve workers a contractor never meant to cover. The injury happens, the carrier asks questions, and the worker who was treated as independent labor suddenly becomes the center of a classification dispute.

The verified brief states that in 2024, the National Institute for Workers Compensation reported that 38% of small contractor claims involved misclassified workers, with average fines of $12,500 per incident on top of the claim cost itself. That is why an injury involving a paid 1099 helper can become much more than a normal workers comp claim.

When a worker gets hurt, the paperwork label matters less than the working relationship.

A practical post-injury approach

After the immediate report, the contractor should stay organized and calm. The right tone matters. Don't accuse the worker of faking. Don't promise coverage decisions the contractor can't make. Don't coach the story.

Instead, keep the file factual. Save texts, daily logs, witness names, and payroll records tied to that worker. If modified duty is available and appropriate under the claim process, document that too. Contractors who stay disciplined after an injury usually protect both the employee and the business better than those who try to improvise.

Smart Loss Control Tactics to Lower Your Future Premiums

A concrete contractor can't eliminate jobsite risk. The contractor can reduce avoidable injuries, make claims less severe, and build a record that supports better pricing over time. That's the practical value of loss control.

Safety programs fail when they live only in a binder. They work when supervisors repeat the same expectations on real crews, with real tasks, before the work starts.

The habits that actually change claim outcomes

For small contractors, the most useful tactics are usually the least glamorous. Weekly toolbox talks. Equipment checks that get logged. PPE enforcement that doesn't get waived when the foreman is busy. Return-to-work planning so an injured employee doesn't disappear from the process.

A concrete flatwork crew offers a clear example. Rebar caps, lifting practices, saw handling, gloves, eye protection, and housekeeping don't look strategic on their own. Together, they reduce the kinds of injuries that create recurring claim patterns.

A strong loss-control routine often includes:

- Short safety talks tied to current work: Discuss trenching this week, not ladder safety from six months ago.

- Supervisor accountability: If foremen ignore PPE, crews will too.

- Written incident follow-up: Every near miss should lead to one practical correction.

- Return-to-work planning: Light duty, yard organization, inventory counts, or shop support can keep a claim from drifting.

Why this affects premium later

The experience modification factor is where safety performance starts showing up financially. A contractor with fewer and less severe claims tends to present differently to the market than a contractor with repeated preventable injuries.

That doesn't mean every injury is avoidable. Construction isn't a clean-room business. It does mean repeated cuts, strains, falls, and hand injuries usually point back to training, supervision, housekeeping, or pace-of-work problems.

For contractors that want a structured outside view of site safety and loss trends, loss control services for contractors are one way to review where procedures are breaking down.

What doesn't work

Posters don't fix a sloppy site. Generic written policies don't help if new hires never hear them. A "be careful out there" culture doesn't stand up after a claim review.

Safety becomes a pricing issue when the same injury pattern keeps coming back.

The contractors who usually improve their workers comp position treat safety like production. They assign responsibility, measure follow-through, and correct drift before it turns into a claim file.

Becoming a Lower-Risk Contractor Starts Now

Well-run contractors don't treat workers comp as a once-a-year purchase. They treat it like part of operations. Hiring, payroll coding, subcontractor onboarding, safety meetings, and audit prep all feed the same system.

That system starts with one basic discipline. Know who needs to be covered. A helper on weekends, a day laborer doing core field work, or a "1099" worker who operates like an employee can create exposure long before anyone files a claim.

What lower-risk contractors do differently

The contractors who usually get cleaner outcomes tend to follow a few habits consistently:

- They classify labor accurately. Office staff isn't field labor, and field labor isn't clerical just because the quote looks better.

- They manage subcontractor documentation early. They don't wait for the audit to find out a certificate is missing.

- They keep records that make sense months later. Payroll, job descriptions, and subcontractor files should still tell the same story at audit time.

- They treat safety as cost control. Fewer preventable injuries usually leads to a healthier account over time.

A plumbing company is a good example. Two service techs, one dispatcher, and a rotating list of excavation subs can look simple from the outside. In practice, that's a business with employee classification exposure, subcontractor certificate exposure, vehicle exposure, and injury reporting exposure all running at once. The contractors who understand that early usually avoid the biggest surprises later.

The real trade-off

Trying to cut workers comp corners can make the initial bill look smaller. Then the actual costs show up somewhere else. In an audit bill, a subcontractor dispute, a denied claim fight, or a jobsite injury involving someone the contractor never meant to put on payroll.

The better trade-off is operational clarity. Correct classifications. Updated certificates. Quick claim reporting. Real supervision. Those choices don't remove risk from contracting, but they make it more controllable.

Workers comp for small business works best when it stops being viewed as a forced expense and starts being managed as part of how the company hires, bids, documents, and supervises work. That is usually the dividing line between the contractor who is constantly reacting and the one who is building a durable business.

A contractor that wants a clearer picture of current workers comp exposure can request a free quote or coverage review from Coverage Axis. A licensed advisor can review payroll setup, class codes, subcontractor certificate handling, and audit risks to help identify where the current program fits the business and where it needs work.